Singapore is ready to take a bite of the fast-growing Asian gaming pie, with an expected US$3 billion in revenue in 2010 that is set to double by 2015, predicts investment bank CLSA.

In a recently published research report, CLSA’s Aaron Fischer, Jon Oh and Huei Suen Ng highlight their reasons for being optimistic about the city-state’s nascent casino industry

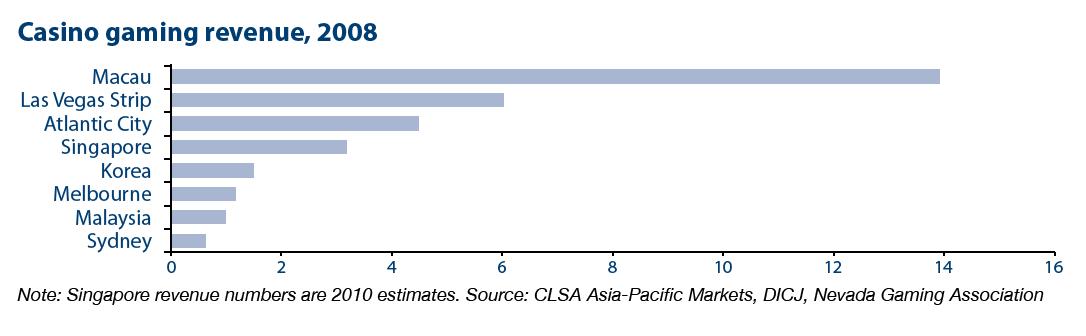

We identify six reasons to be bullish on the Singapore gaming sector and six features that the market has yet to price in. These factors will drive gaming revenue of US$3 billion next year (about 23% that of Macau), growing at 12% per annum thereafter. Lower gaming taxes add to the appeal of Singapore as a VIP gaming market. The local population’s appetite for gambling will complement the tourist segment (60% of total casino visitors), with Indonesia, Malaysia and Thailand supplying the bulk of overseas customers.

Resorts World is for everyone

We estimate a 46% market share for Genting Singapore’s Resorts World, which targets families. Gaming Ebitda [earnings before interest, taxes, depreciation and amortisation] margin should be around 40% in 2010 (versus 22% in Macau, which is subject to higher gaming taxes). Our model conservatively assumes a 1.3% junket-commission rate for the VIP market, which will contribute to 40% of total revenue.

A top-five theme park in Asia

Adding to Resorts World’s winning hand are a Universal Studios theme park, hotels and retail space, making it an entertainment venue for a wide audience. These non-gaming components will add a further S$160 million to 11CL Ebitda. Based on our estimates of four million visitors in 2010 and 4.5 million in 2011, Universal Studios will become the fifth most popular theme park in Asia, and among the top 15 globally, in two years.

Resort Ebitda drives target

We expect Resorts World’s Ebitda to grow 12% per annum in the medium term, with potential upside to our Ebitda-margin estimate as it should achieve scale efficiencies over time. Our 2011 earnings estimate is 75% above consensus given our more bullish view on the Singapore gaming sector. We forecast a 2011 EV/Ebitda [Enterprise Value/Ebitda] of 12 times for the resort, based on peer multiples. This is the key contributor to our S$1.10 sum-of-parts target price for the stock.

RelatedPosts