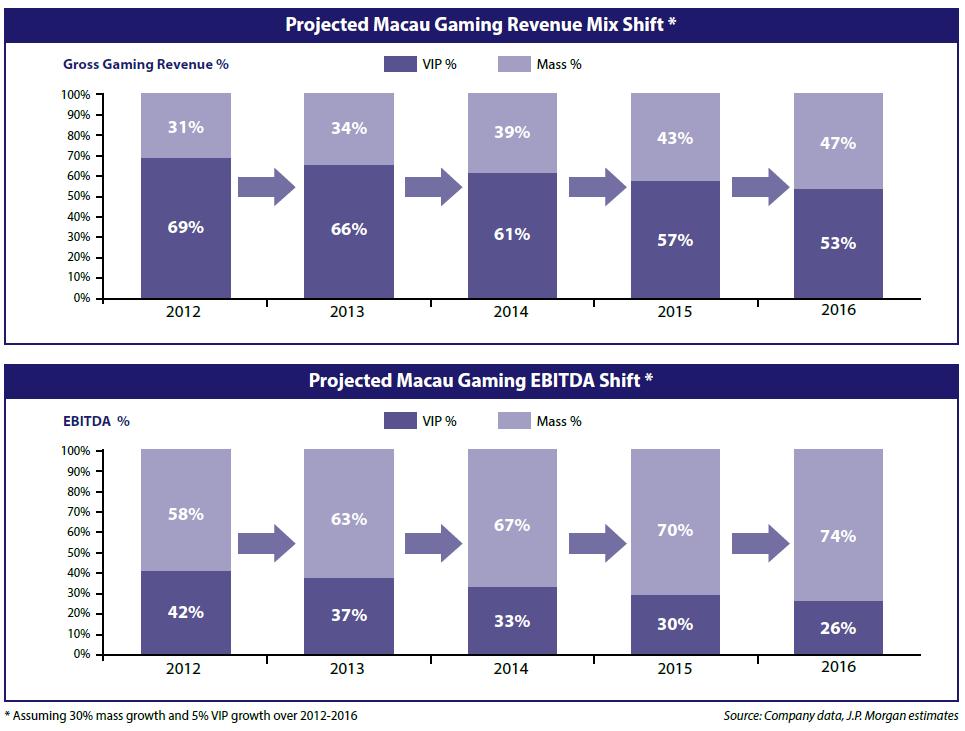

The inexorable growth of Macau’s mass market—and the premium mass in particular— is revving up industry profitability. If current trends continue, the mass looks set to deliver three-quarters of the city’s gaming profits by 2016

The ban on low-cost package tours from mainland China to Macau that came into effect on 1st October coincided with a 31.7% year-on-year surge in Macau’s gross gaming revenue last month to MOP36.5 billion (US$4.6 billion). Although part of the exceptional growth in October was the result of an easy comp— with revenue up a mere 3.2% in the year- ago month—it seems likely that by keeping away some of the lower-spending crowds during the week-long holiday period around China National Day on 1st October, the ban cleared the way for premium mass players to significantly lift the average bet size in the city.

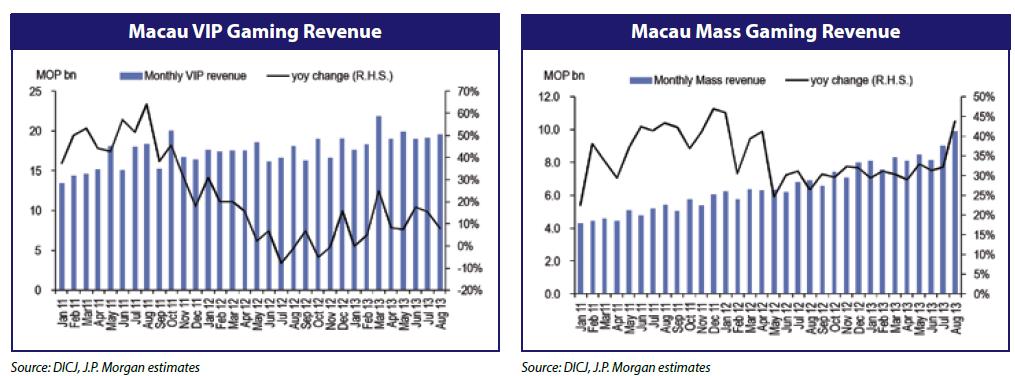

Macau’s total gaming revenue rose 17% year on year in the third quarter of 2013 to MOP89.2 billion ($11.1 billion), with VIP revenue, which constituted 65% of the total, up 13% and mass revenue, accounting for 31% of the total, rising 37%. The remaining 4% was made up of slot revenue, which grew 13% in the quarter.

Since the end of 2011, the growth of the high-margin mass market has comfortably outstripped that of the dominant but much lower-margin VIP sector, and the result is that local casinos—and particularly the more mass-market-focused ones—are seeing profitability increase by a greater degree than the headline revenue number. Macau’s most mass-market focused operator, Sands China, for example, reported a 42.7% increase in Q3 revenue to $2.3 billion and a 62.8% jump in adjusted EBITDA to $785 million.

The increasing contribution of the mass market is also improving the earnings profile of Macau operators, according to J.P. Morgan Leisure and Gaming analyst Kenneth Fong. In a recent report, Mr Fong highlighted: “From an earnings quality perspective, the cash-driven mass market revenue is also more sustainable and less cyclical than the receivables-driven VIP segment. One of the reasons why investors refrain from assigning a higher valuation to the Macau gaming sector is its reliance on credit-driven VIP revenue, whose growth is hard to predict. The increased contribution from mass market growth should give investors improved earnings visibility.”

If the mass market continues growing at 25% and VIP at a slower 5%, “The revenue mix would become 50/50 between VIP and mass as soon as 2016,” according to Mr Fong. Furthermore, “Due to the profit margin difference between the two segments (VIP 10% vs. mass 35-40%), the VIP segment now contributes only 42% of EBITDA, despite contributing 70% of the top line. In our scenario discussed above, the EBITDA contribution from VIP could decline to only 25% in 2016.”

J.P. Morgan’s latest forecast calls for 16% growth in Macau gaming revenue this year, which translates to headline gaming revenue of MOP354 billion ($44.3 billion). In a recent report, Mr Fong adds: “Looking ahead, we expect 2014 and 2015 gross gaming revenue to grow by 16% (up from 13%) and 17%, respectively. Our growth estimates are at the high end of the Street’s assumptions, as we have more optimistic VIP gaming revenue forecasts.

Market Shares

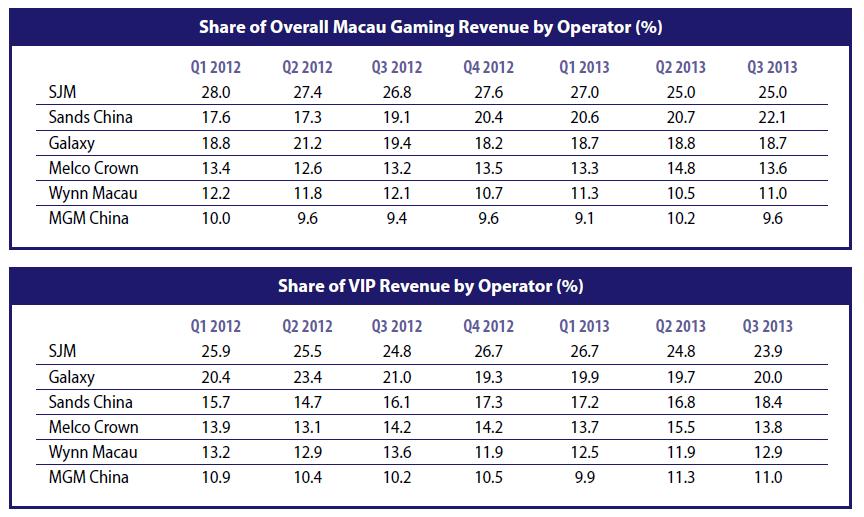

Following the liberalization of Macau’s casino industry in 2002, allowing the entry of five new operators, the market share lead of erstwhile monopoly operator SJM has been steadily eroded.

SJM still commands the largest share of Macau gaming revenue, though Sands China is hard on its heels. SJM’s share held steady at 25% between the second and third quarters, though Sands China managed to increase its share from 20.7% in Q2 to 22.1% owing to its dominance in the fast-growing mass market. Sands’ gain was largely the result of loss of share by Melco Crown Entertainment.

Melco Crown Entertainment’s City of Dreams

Sands China also saw the largest gain in its share of VIP revenue in the third quarter, while Melco Crown experienced the greatest loss. Notably, while SJM suffered an erosion in its share of VIP revenue, this was the result of an especially unlucky quarter in its VIP segment— its 3Q VIP win rate of 2.65% was the lowest among the six operators. The industry-wide average was 3.12%, Sands China achieved 3.67%, Galaxy Entertainment Group, 3.05%, Wynn Macau, 3.38%, MGM China Holdings, 3.02% and Melco Crown got 2.96% at Altira and 3.79% at City of Dreams.

RelatedPosts

Discounting the luck factor by considering VIP rolling chip turnover by operator, it seems Melco Crown indisputably lost ground in the VIP sector in the third quarter, while SJM could actually have improved its standing in the segment if it wasn’t for an unlucky quarter. Sands China has enjoyed the biggest continuous gains in its share of VIP revenue since the beginning of 2012.

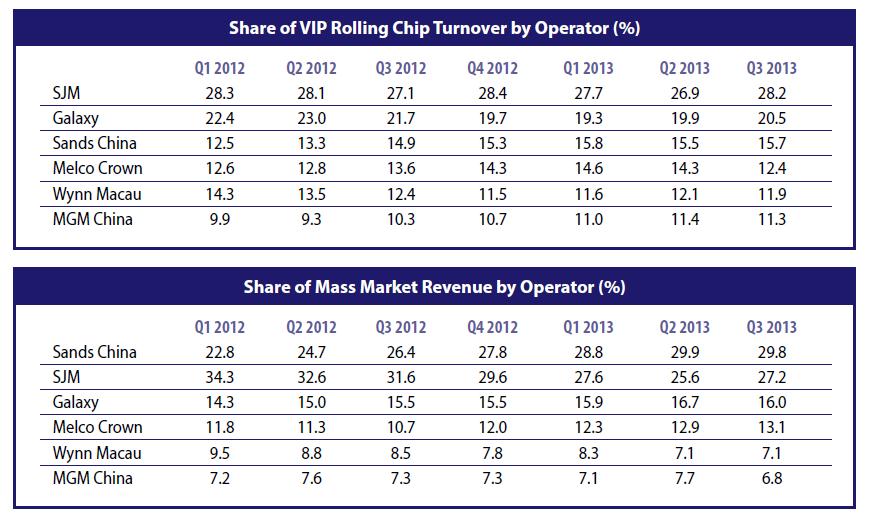

SJM’s share of mass revenue managed to rebound from a nadir of 25.6% in Q2 to 27.2% in Q3.

SJM’s share of mass revenue managed to rebound from a nadir of 25.6% in Q2 to 27.2% in Q3.

SJM’s share of mass market revenue has fallen steadily since last year in the face of significant capacity expansion by Sands China at Sands Cotai Central and as Galaxy and Melco Crown continue to ramp up their premium-mass businesses. Still, SJM’s share of mass revenue managed to rebound from a nadir of 25.6% in Q2 to 27.2% in Q3.

Sands China unseated SJM as the market leader in mass revenue in the first quarter of this year, maintaining that lead into the third quarter with a 29.8% share. Meanwhile, MGM China Holdings lagged the field with a 6.8% share, having been overtaken in the quarter by Wynn Macau.