Macau’s 2014 growth is set to outperform consensus expectations, according to Morgan Stanley

“Our estimates are ahead of consensus by 3-10% for 2014 EBITDA. We also believe that operating leverage could mean 13-39% year-on-year EBITDA growth in 2014, versus the consensus of 9-27%,” wrote Morgan Stanley’s Praveen Choudhary in a recent report.

The report gives an overall growth figure of 18.3% (2014 consensus is 12.3%), revised significantly upwards from the company’s original forecast of 13%, giving a gross gaming revenue (GGR) figure of US$53 billion for 2014. According to the report, given that annualizing Q4 2013 revenue into 2014 would result in 11%, positive revision is very likely.

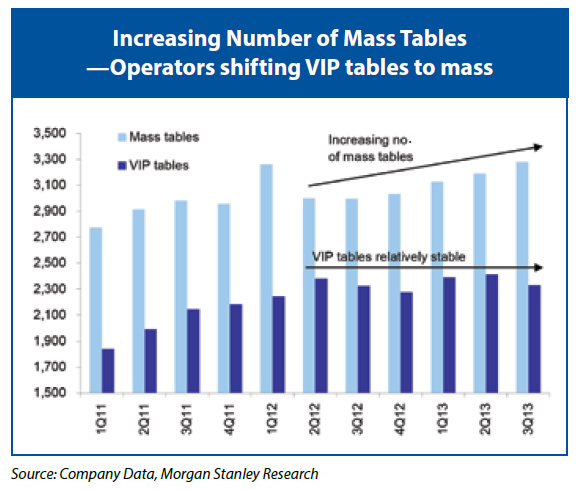

The figure is comprised of 13% growth in VIP gaming and 28% in mass, thus the optimistic forecast for increased operating leverage.

Key Factors

The report’s case for the upswing in mass spending is based in the main on three factors. The first is movement of tables from VIP to mass, with the proliferation of premium mass to other casinos after successful implementation by MPEL/MGM expected to have an impact.

Second, Macau is seeing sustained visitation growth, up 4.5% year on year through November. “We expect 7% visitor growth in 2014, driven by infrastructure improvements, extension of the Individual Visit Scheme, Rmb appreciation, and the wealth effect,” said the report.

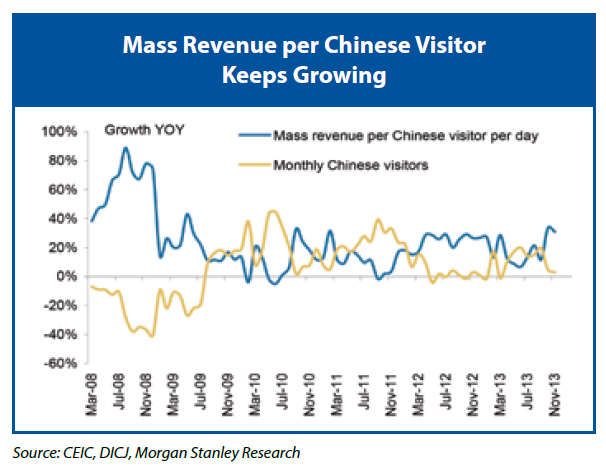

Finally, spending per visitor remains in double figures, which also pushed up mass table yields to 28% in 2012/13 (the 2013 figure is an estimate). The company expects 18% year-on-year growth in mass table yield.

Caution Required

However, there is also reason to be cautious. The number of hotel rooms is expected to grow by only 3% in 2014, meaning that growth will need to be driven by yield per room per visitor, while similarly, constraints on the overall number of tables mean that revenue per table will need to grow.

Ameliorating the latter concern somewhat is the restriction on tour groups from 1st October, 2013, which has seen a decrease in the number of low-quality visitors and has helped to push spending per visitor higher.

VIP Yields to Increase

VIP table yield is also set to increase, with drivers including accelerated liquidity and an enlarging mainland customer base; moreover, according to the report, given the 18% year-on-year growth in Q4 2013, 13% for 2014 should not be a stretch. According to the report, further upwards movement could come from VIP growing faster than expected.

This will be partially offset by a 2% year-on-year decline in the number of VIP tables as operators gradually move VIP tables to mass, and downside risks remain. Competition from other jurisdictions weighs, while the report also points to the impact of a potential expansion of the smoking ban.

Constraints on 2015

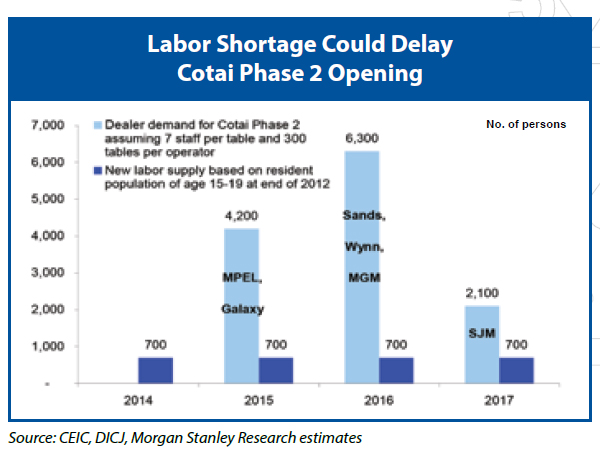

Looking further ahead, capacity constraint will remain an issue until the opening of Cotai phase 2 in mid-2015. More seriously, however a shortage of labor could even delay this development; projected demand combined with the tight labor market and requirements such as the ban on non-locals working as dealers could see a shortfall in the thousands.

RelatedPosts

Infrastructure development is not expected to be a growth factor in the near term, with the light rail delayed and the Taipa ferry terminal not increasing the amount of mainland tourists.

Strong Q4 2013 the Basis

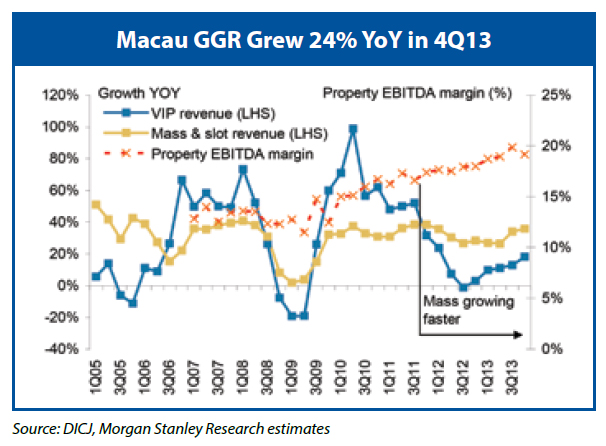

“Our revision is based on stronger-than-expected 4Q13 revenue of MOP$110bn, representing growth of 12% quarter on quarter and 24% year on year,” the report stated.

In the quarter, 35% of revenue came from the mass segment, representing a gain of 11% quarter on quarter and 34% year on year. A slightly weaker luck factor for the quarter saw VIP revenue grow by 19% year on year versus 21% year-on-year growth for VIP roll.

The quarter also saw operators’ EBITDA per table per day converge, most being within the US$5,000-$7,000 range.